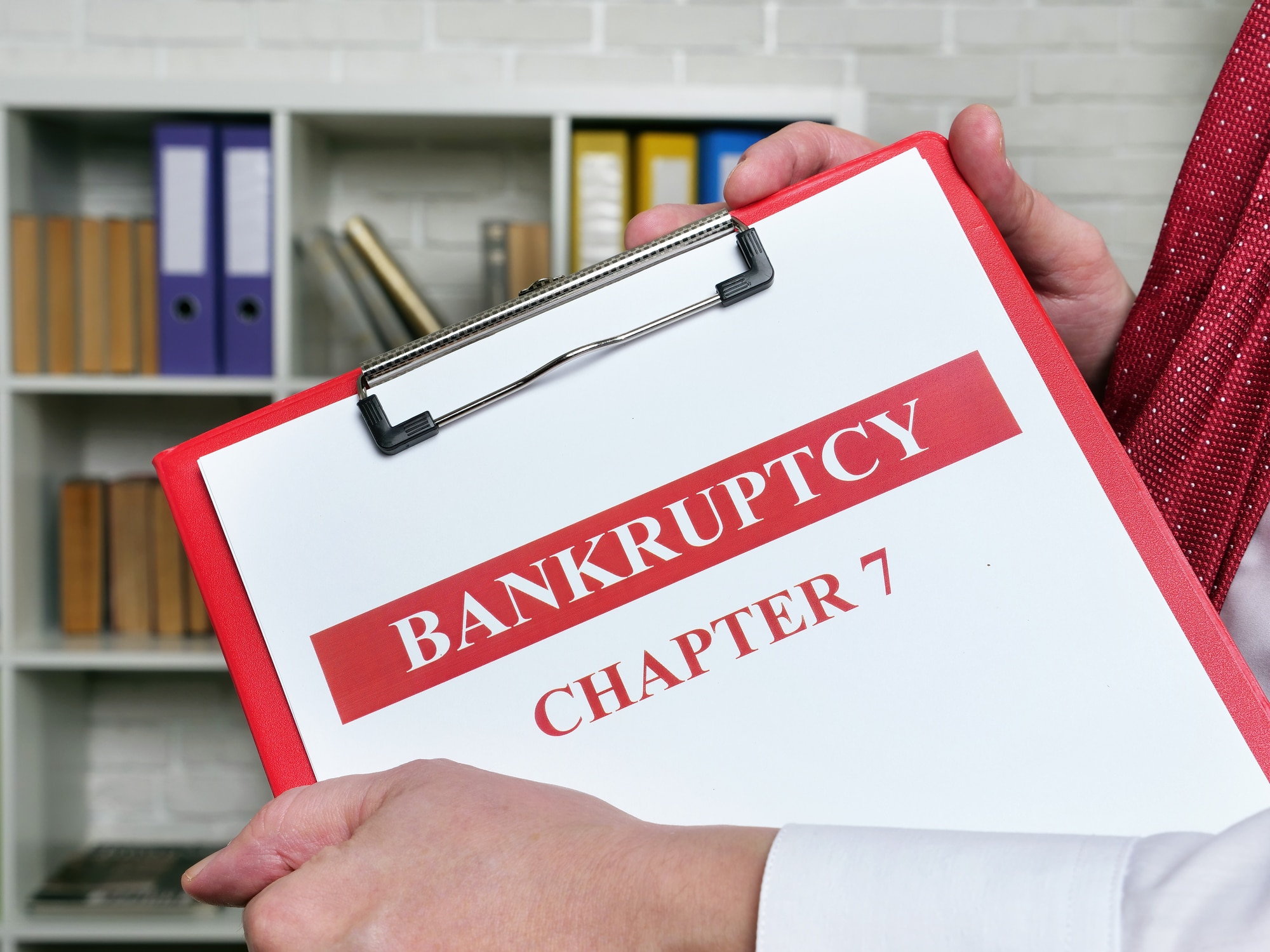

Why You Should Consider Chapter 7 Bankruptcy

Chapter 7 bankruptcy is much different from Chapter 13 bankruptcy in that it does not involve filing a repayment plan. Instead, the trustee for the bankruptcy will gather and sell the debtor’s assets that are not exempt and use the proceeds of the sales to pay any creditors according to the Bankruptcy Code provisions. Some of the property could be subject to mortgages and liens that pledge certain property to creditors. The Bankruptcy Code allows the debtor to keep some exempt property, but the remaining assets will be liquidated by the trustee. You need to understand that filing a Chapter 7 bankruptcy can result in the loss of some of your property.

Eligibility Requirements for Chapter 7 Bankruptcy

To qualify for a Chapter 7 bankruptcy under the Bankruptcy Code, the debtor must be either an individual, partnership, corporation or some other classification of business. The debtor will be subjected to the means test if he or she is an individual debtor, and whether the debtor is eligible or not will depend on his or her debts and whether they are insolvent or solvent.

You may also not qualify for bankruptcy if a prior petition for bankruptcy has been dismissed in the preceding 180 days and you failed to appear in court, comply with orders of the court, or chose to voluntarily dismiss the case when creditors attempted to recover property that had liens on them.

In addition, you will also not be allowed to file for Chapter 7 bankruptcy unless you have received credit counseling from an approved agency within 180 days of filing for bankruptcy. There are certain emergency exceptions where the bankruptcy trustee may determine that there are not approved agencies that are able to provide the necessary counseling. If, however, a debt management plan is developed, that plan must be filed with the court.

Alternatives to Chapter 7 Bankruptcy

You should be aware that there are sometimes alternatives available for financial relief besides Chapter 7 bankruptcy. For example, if you are engaged in a business, you may be able to file for relief under Chapter 11 of the Bankruptcy Code. Individual debtors that have consistent income may be able to qualify for debt relief under Chapter 13 of the Bankruptcy Code. This will provide you with the option to save your home by allowing you to catch up on any past due mortgage payments and avoid foreclosure.

If your monthly income is more than the state median, you will be required to take a means test to determine if you are eligible for Chapter 7 bankruptcy or if you will be required to file Chapter 13 instead. The median income in Georgia is $51,037 according to the U.S. Census Bureau. You should also be aware that agreements made with creditors outside of court may provide an alternative to filing for bankruptcy.

Seek the Counsel of an Experienced Bankruptcy Attorney

Ultimately the primary purpose of filing for bankruptcy is to discharge some of your debts and give you a fresh start. Depending on your situation, Chapter 7 bankruptcy may be the best option for you, or there may be other alternatives. That is where an experienced bankruptcy attorney steps in. The attorneys at Cornwell Law Firm have years of experience helping their clients seek financial relief through bankruptcy and they can help you too. Contact us today to schedule a free consultation and take your first steps to financial freedom.

Muchas gracias. ?Como puedo iniciar sesion?

I have not checked in here for some time as I thought it was getting boring, but the last several posts are good quality so I guess I’ll add you back to my everyday bloglist. You deserve it my friend 🙂

… [Trackback]

[…] Find More to that Topic: cornwellbankruptcy.com/chapter-7/chapter-7-bankruptcy/ […]

You have remarked very interesting details! ps nice web site.

I was examining some of your posts on this website and I believe this website is real informative! Keep on putting up.

Very interesting topic, regards for putting up.

… [Trackback]

[…] There you will find 73910 more Information to that Topic: cornwellbankruptcy.com/chapter-7/chapter-7-bankruptcy/ […]

… [Trackback]

[…] Find More Info here on that Topic: cornwellbankruptcy.com/chapter-7/chapter-7-bankruptcy/ […]

… [Trackback]

[…] Information on that Topic: cornwellbankruptcy.com/chapter-7/chapter-7-bankruptcy/ […]

… [Trackback]

[…] Read More on that Topic: cornwellbankruptcy.com/chapter-7/chapter-7-bankruptcy/ […]

… [Trackback]

[…] Find More Information here on that Topic: cornwellbankruptcy.com/chapter-7/chapter-7-bankruptcy/ […]

… [Trackback]

[…] Read More here to that Topic: cornwellbankruptcy.com/chapter-7/chapter-7-bankruptcy/ […]

… [Trackback]

[…] Here you will find 76262 more Info on that Topic: cornwellbankruptcy.com/chapter-7/chapter-7-bankruptcy/ […]

It?¦s really a cool and useful piece of information. I am happy that you simply shared this useful information with us. Please stay us informed like this. Thank you for sharing.

… [Trackback]

[…] Here you can find 4392 additional Information on that Topic: cornwellbankruptcy.com/chapter-7/chapter-7-bankruptcy/ […]

You actually make it seem really easy with your presentation however I to find this matter to be actually something which I believe I might by no means understand. It sort of feels too complicated and extremely large for me. I am looking ahead in your subsequent submit, I¦ll try to get the hang of it!

I truly appreciate this post. I?¦ve been looking all over for this! Thank goodness I found it on Bing. You’ve made my day! Thanks again

… [Trackback]

[…] Info to that Topic: cornwellbankruptcy.com/chapter-7/chapter-7-bankruptcy/ […]

Hi my friend! I wish to say that this article is amazing, great written and include approximately all vital infos. I would like to see more posts like this .

I챠m impressed, I have to admit. Rarely do I encounter a blog that챠s both equally educative and engaging, and let me tell you, you’ve hit the nail on the head. The problem is an issue that too few folks are speaking intelligently about. I am very happy that I found this during my search for something regarding this.

Keep functioning ,impressive job!

I am always thought about this, regards for posting.

… [Trackback]

[…] Find More on that Topic: cornwellbankruptcy.com/chapter-7/chapter-7-bankruptcy/ […]

you have a great blog here! would you like to make some invite posts on my blog?

Thank you for every one of your labor on this web site. Betty loves participating in internet research and it’s really simple to grasp why. Many of us hear all about the dynamic medium you make insightful guides by means of this web site and as well foster participation from visitors on that subject then our favorite child is certainly discovering a lot. Take pleasure in the rest of the new year. You have been conducting a dazzling job.

Please let me know if you’re looking for a article author for your weblog. You have some really good posts and I feel I would be a good asset. If you ever want to take some of the load off, I’d really like to write some articles for your blog in exchange for a link back to mine. Please blast me an e-mail if interested. Kudos!

I always was interested in this subject and stock still am, thanks for putting up.

… [Trackback]

[…] Find More Information here to that Topic: cornwellbankruptcy.com/chapter-7/chapter-7-bankruptcy/ […]

… [Trackback]

[…] Find More here on that Topic: cornwellbankruptcy.com/chapter-7/chapter-7-bankruptcy/ […]

… [Trackback]

[…] Read More here to that Topic: cornwellbankruptcy.com/chapter-7/chapter-7-bankruptcy/ […]

Hey would you mind sharing which blog platform you’re working with?

I’m looking to start my own blog soon but I’m having a difficult time choosing between BlogEngine/Wordpress/B2evolution and

Drupal. The reason I ask is because your design and style seems different then most blogs and I’m looking for something

completely unique. P.S Sorry for being off-topic but I

had to ask!

… [Trackback]

[…] Read More to that Topic: cornwellbankruptcy.com/chapter-7/chapter-7-bankruptcy/ […]

Great, thanks for sharing this article post. Want more.

Hello there! I like your content, keep sharing it. You’re so professional at it. Also check out my website, I’m sharing some good stuff. dil nedir

… [Trackback]

[…] Find More to that Topic: cornwellbankruptcy.com/chapter-7/chapter-7-bankruptcy/ […]

… [Trackback]

[…] Read More to that Topic: cornwellbankruptcy.com/chapter-7/chapter-7-bankruptcy/ […]

… [Trackback]

[…] There you can find 86548 more Information to that Topic: cornwellbankruptcy.com/chapter-7/chapter-7-bankruptcy/ […]

… [Trackback]

[…] Info on that Topic: cornwellbankruptcy.com/chapter-7/chapter-7-bankruptcy/ […]

I like your writing style really enjoying this website .

… [Trackback]

[…] Find More Info here on that Topic: cornwellbankruptcy.com/chapter-7/chapter-7-bankruptcy/ […]

… [Trackback]

[…] Read More on on that Topic: cornwellbankruptcy.com/chapter-7/chapter-7-bankruptcy/ […]

… [Trackback]

[…] Info to that Topic: cornwellbankruptcy.com/chapter-7/chapter-7-bankruptcy/ […]

I got this site from my pal who informed me on the topic of this web page and now this time I am visiting this site and reading very informative content at this time.

Greetings! Very useful advice within this article! It’s the little changes that will make the biggest changes.Thanks for sharing!

Hi there! I like your content, keep it going. You’re so good at it. Also check out my blog, I’m sharing some good content. google password reset

Hello there! I like your content, keep it going. You’re really good at it. Also check out my website, I’m posting some good stuff. reset gmail password

Hi there! I love your post, keep sharing it. You’re really good at it. Also check out my blog, I’m sharing some amazing content. recovery google account

Hey there! I love your article, keep sharing it. You’re really professional at it. Also check out my blog, I’m sharing some good stuff. forgot gmail password

Hey there! I like your post, keep doing it. You’re really professional at it. Also check out my blog, I’m sharing some good stuff. gmail account recovery phone number

Hi there! I love your post, keep it up. You’re really professional at it. Also check out my website, I’m posting some amazing stuff. gmail recovery email

Hi there! I like your post, keep sharing it. You’re so professional at it. Also check out my blog, I’m sharing some amazing content. forgot my gmail password

Hello there! I love your content, keep sharing it. You’re really good at it. Also check out my website, I’m sharing some good stuff. google account recovery phone number

Hi there! I love your article, keep sharing it. You’re really good at it. Also check out my website, I’m posting some amazing stuff. forgot my gmail password

Hello there! I like your post, keep it going. You’re so professional at what you’re doing. Also check out my website, I’m posting some good stuff. google recovery password

Hello there! I like your post, keep it going. You’re so good at it. Also check out my website, I’m posting some amazing stuff. gmail account recovery page

Hi there! I love your article, keep doing it. You’re so professional at it. Also check out my blog, I’m posting some amazing content. recover gmail account without phone number

Hey there! I like your article, keep doing it. You’re so good at what you’re doing. Also check out my website, I’m sharing some amazing stuff. get free robux

Hi there! I love your post, keep sharing it. You’re really good at what you’re doing. Also check out my website, I’m sharing some amazing content. get free robux

Hi there! I like your post, keep doing it. You’re really good at it. Also check out my blog, I’m posting some good stuff. free robux app

Hi there! I like your post, keep it going. You’re really good at what you’re doing. Also check out my blog, I’m sharing some good content. roblox free robux

Hey there! I love your content, keep it up. You’re so good at it. Also check out my website, I’m posting some good content. free robux generator

Hey there! I love your post, keep it going. You’re so good at it. Also check out my website, I’m sharing some amazing content. roblox free robux

Hello there! I like your article, keep doing it. You’re so professional at it. Also check out my website, I’m sharing some good content. free robux easy

Hey there! I love your content, keep it up. You’re so professional at it. Also check out my website, I’m sharing some good content. how to get free robux

Hey there! I like your content, keep it up. You’re so professional at it. Also check out my website, I’m sharing some amazing content. dilin anlamı

Hi there! I love your content, keep it up. You’re so professional at what you’re doing. Also check out my blog, I’m sharing some good content. okur yazarlık

Hi there! I love your article, keep it up. You’re really professional at it. Also check out my website, I’m posting some amazing stuff. dil ne demek

Hi there! I like your post, keep it going. You’re so good at what you’re doing. Also check out my blog, I’m posting some good stuff. dil nedir tanımı

Hi there! I like your content, keep it up. You’re so professional at what you’re doing. Also check out my website, I’m posting some amazing content. dil ne demek

Hello there! I like your content, keep sharing it. You’re so good at what you’re doing. Also check out my blog, I’m posting some amazing content. okur yazarlık

Hey there! I like your article, keep it going. You’re really professional at what you’re doing. Also check out my website, I’m sharing some amazing content. okuryazar

Hey there! I love your post, keep sharing it. You’re so good at it. Also check out my website, I’m sharing some amazing stuff. fpog blogspot

It is very great thing!

You made some first rate points there. I looked on the internet for the problem and located most people will go together with together with your website.

I like this post, enjoyed this one thankyou for posting.

Good article. I absolutely appreciate this website. Keep writing!|

Hi there it’s me, I am also visiting this web page daily, this site is truly nice and the people are actually sharing pleasant thoughts.|

Nice post. I was checking continuously this blog and I am impressed! Very useful information specially the last part 🙂 I care for such information much. I was looking for this particular information for a long time. Thank you and best of luck.|

Post writing is also a excitement, if you know afterward you can write or else it is complicated to write.|

It’s perfect time to make a few plans for the long run and it is time to be happy. I have read this publish and if I could I want to counsel you few interesting issues or advice. Maybe you could write subsequent articles relating to this article. I want to learn even more things approximately it!|

Great blog! Is your theme custom made or did you download it from somewhere? A design like yours with a few simple adjustements would really make my blog shine. Please let me know where you got your theme. With thanks|

Hello, Neat post. There’s a problem along with your website in internet explorer, may check this? IE nonetheless is the market leader and a big component to other people will miss your great writing due to this problem.|

Im thankful for the post.

hey there and thank you for your info – I have definitely picked up something new from right here. I did however expertise some technical points using this site, as I experienced to reload the website lots of times previous to I could get it to load correctly. I had been wondering if your web hosting is OK? Not that I am complaining, but sluggish loading instances times will very frequently affect your placement in google and can damage your quality score if advertising and marketing with Adwords. Anyway I’m adding this RSS to my email and can look out for much more of your respective interesting content. Make sure you update this again soon.|

Buy Nimesulide online

Hi, i think that i saw you visited my web site so i came to

“return the favor”.I am trying to find things to enhance my website!I suppose its ok to

use some of your ideas!!

Hello my friend! I want to say that this post is awesome, nice written and include almost all vital infos. I’d like to see more posts like this.

Thank you, I have just been looking for info approximately this subject for a long time and yours is the best I have came upon till now. However, what about the conclusion? Are you certain concerning the supply?

medunitsa.ru Medunitsa.ru

Фильм смотрите бесплатно на Filmix..

Вот смотреть онлайн в хорошем качестве бесплатно фильмы.

Где смотреть онлайн бесплатно

Thank you for every other great post. The place else may just anybody get that type of information in such an ideal approach of writing? I have a presentation subsequent week, and I’m on the look for such information.

Найти психолога в Москве

An interesting discussion is worth comment. I think that you should write more on this topic, it might not be a taboo subject but generally people are not enough to speak on such topics. To the next. Cheers

Thank you for the good writeup. It in fact used to be a leisure account it. Look complex to far brought agreeable from you! However, how can we keep up a correspondence?

Via my investigation, shopping for electronics online can for sure be expensive, although there are some tricks and tips that you can use to help you get the best products. There are usually ways to uncover discount discounts that could make one to come across the best consumer electronics products at the lowest prices. Good blog post.

I like the helpful info you supply to your articles. I will bookmark your blog and check once more here frequently. I’m slightly certain I?ll be told a lot of new stuff proper here! Good luck for the next!

I appreciate, cause I found just what I was looking for. You have ended my 4 day long hunt! God Bless you man. Have a nice day. Bye

I like this site because so much utile material on here : D.

454

Please tell me more about this. May I ask you a question?

Thank you for your help. I must say you’ve been really helpful to me.

Thank you for providing me with these article examples. May I ask you a question?

Thank you for posting this post. I found it extremely helpful because it explained what I was trying to say. I hope it can help others as well.

Thank you for your articles. I find them very helpful. Could you help me with something?

You’ve been terrific to me. Thank you!

Thank you for sharing this article with me. It helped me a lot and I love it.

Thank you for your excellent articles. May I ask for more information?

I really enjoyed reading your post and it helped me a lot

How can I find out more about it?

You really helped me by writing this article. I like the subject too.

Can you write more about it? Your articles are always helpful to me. Thank you!

Thank you for posting this. I really enjoyed reading it, especially because it addressed my question. It helped me a lot and I hope it will help others too.

I will right away grab your rss feed as I can’t find your e-mail subscription link or newsletter service. Do you have any? Kindly let me know so that I could subscribe. Thanks.

Thanks for your post on this site. From my own experience, often times softening right up a photograph could provide the photography with a little bit of an creative flare. Many times however, the soft clouds isn’t what exactly you had at heart and can usually spoil an otherwise good photograph, especially if you intend on enlarging it.

I am not really great with English but I line up this real easy to read .

You should take part in a contest for one of the best blogs on the web. I will recommend this site!

Hey there! This is kind of off topic but I need some help from an established blog. Is it difficult to set up your own blog? I’m not very techincal but I can figure things out pretty fast. I’m thinking about creating my own but I’m not sure where to start. Do you have any points or suggestions? Thank you

At this time it looks like Movable Type is the preferred blogging platform available right now. (from what I’ve read) Is that what you are using on your blog?

Pretty section of content. I just stumbled upon your site and in accession capital to assert that I acquire actually enjoyed account your blog posts. Anyway I will be subscribing to your augment and even I achievement you access consistently fast.

Great line up. We will be linking to this great article on our site. Keep up the good writing.

Fantastic site. A lot of useful information here. I’m sending it to a few friends ans also sharing in delicious. And of course, thanks for your sweat!

How do I find out more?

Hi there, I found your blog via Google while searching for a related topic, your website came up, it looks good. I have bookmarked it in my google bookmarks.

Thanks for your posting. Another factor is that being photographer requires not only difficulty in recording award-winning photographs and also hardships in getting the best digital camera suited to your requirements and most especially hardships in maintaining the grade of your camera. This is very correct and evident for those photographers that are directly into capturing the particular nature’s eye-catching scenes – the mountains, the forests, the wild and the seas. Going to these amazing places absolutely requires a digital camera that can meet the wild’s unpleasant area.

Thanks for posting. I really enjoyed reading it, especially because it addressed my issue. It helped me a lot and I hope it will help others too.

There are actually loads of details like that to take into consideration. That may be a great point to deliver up. I supply the thoughts above as common inspiration however clearly there are questions like the one you deliver up the place crucial thing will be working in sincere good faith. I don?t know if finest practices have emerged round things like that, however I am certain that your job is clearly identified as a good game. Both boys and girls really feel the impression of just a second’s pleasure, for the rest of their lives.

I will immediately grab your rss feed as I can not find your e-mail subscription link or e-newsletter service. Do you’ve any? Please let me know in order that I could subscribe. Thanks.

I feel this is one of the so much significant information for me. And i’m satisfied reading your article. But should observation on some general things, The site style is perfect, the articles is in reality excellent : D. Excellent job, cheers

I would like to thank you for the efforts you’ve put in writing this site. I am hoping the same high-grade website post from you in the upcoming as well. In fact your creative writing abilities has inspired me to get my own web site now. Actually the blogging is spreading its wings quickly. Your write up is a great example of it.

Hi, Neat post. There is a problem with your web site in internet explorer, would test this? IE still is the market leader and a good portion of people will miss your excellent writing because of this problem.

Spot on with this write-up, I truly assume this web site needs much more consideration. I’ll most likely be once more to learn way more, thanks for that info.

933

Great write-up, I?m regular visitor of one?s web site, maintain up the nice operate, and It’s going to be a regular visitor for a long time.

This is a very good tips especially to those new to blogosphere, brief and accurate information… Thanks for sharing this one. A must read article.

Great line up. We will be linking to this great article on our site. Keep up the good writing.

I?m not sure where you’re getting your info, but great topic. I needs to spend some time learning more or understanding more. Thanks for wonderful info I was looking for this information for my mission.

I’m really enjoying the design and layout of your site. It’s a very easy on the eyes which makes it much more enjoyable for me to come here and visit more often. Did you hire out a designer to create your theme? Fantastic work!

Thanks for another excellent article. Where else may anybody get that kind of info in such a perfect approach of writing? I have a presentation next week, and I’m on the look for such info.

2

323

wonderful post, very informative. I wonder why the other specialists of this sector do not notice this. You should continue your writing. I’m sure, you’ve a great readers’ base already!

When I initially commented I clicked the “Notify me when new comments are added” checkbox and now each time a comment is added I get several emails with the same comment. Is there any way you can remove me from that service? Thanks a lot!

Thanks for your tips. One thing we’ve noticed is the fact banks plus financial institutions are aware of the spending behavior of consumers and also understand that most people max out their own credit cards around the trips. They smartly take advantage of this specific fact and commence flooding a person’s inbox along with snail-mail box by using hundreds of 0 APR credit card offers immediately after the holiday season closes. Knowing that in case you are like 98 of American public, you’ll soar at the opportunity to consolidate credit card debt and move balances to 0 interest rates credit cards.

I?¦ve learn several just right stuff here. Certainly worth bookmarking for revisiting. I wonder how a lot effort you place to create any such excellent informative site.

Вампиры средней полосы 2 сезон 2 серия

F*ckin? tremendous issues here. I?m very glad to see your post. Thank you a lot and i’m having a look ahead to touch you. Will you please drop me a mail?

Your articles are incredibly helpful to me. Thank you! May I request more information?

There is no doubt that your post was a big help to me. I really enjoyed reading it.

An attention-grabbing discussion is worth comment. I think that you must write extra on this topic, it won’t be a taboo subject but generally persons are not sufficient to talk on such topics. To the next. Cheers

Also a thing to mention is that an online business administration program is designed for scholars to be able to efficiently proceed to bachelor’s degree education. The Ninety credit education meets the other bachelor education requirements and when you earn the associate of arts in BA online, you will have access to the modern technologies in this field. Some reasons why students have to get their associate degree in business is because they’re interested in this area and want to receive the general training necessary just before jumping right into a bachelor education program. Many thanks for the tips you really provide in the blog.

Thank you for your excellent articles. May I ask for more information?

You’ve been very helpful to me. Thank you!

Thanx for the effort, keep up the good work Great work, I am going to start a small Blog Engine course work using your site I hope you enjoy blogging with the popular BlogEngine.net.Thethoughts you express are really awesome. Hope you will right some more posts.

Thank you for your post. I liked reading it because it addressed my issue. It helped me a lot and I hope it will help others too.

I always find your articles very helpful. Thank you!

Thank you for posting this. I really enjoyed reading it, especially because it addressed my question. It helped me a lot and I hope it will help others too.

Thanks for your publication. I would also love to say this that the very first thing you will need to conduct is determine whether you really need fixing credit. To do that you simply must get your hands on a replica of your credit file. That should not be difficult, since government makes it necessary that you are allowed to acquire one free of charge copy of your actual credit report yearly. You just have to request the right individuals. You can either look at website for your Federal Trade Commission or maybe contact one of the major credit agencies right away.

F*ckin? awesome things here. I am very glad to see your post. Thanks a lot and i am looking forward to contact you. Will you please drop me a mail?

Great blog! I am loving it!! Will be back later to read some more. I am taking your feeds also

Your articles are extremely helpful to me. May I ask for more information?

Please provide me with more details on the topic

Thanks for the tips you reveal through this web site. In addition, several young women that become pregnant never even attempt to get medical insurance because they fear they couldn’t qualify. Although many states right now require that insurers give coverage irrespective of the pre-existing conditions. Charges on these guaranteed programs are usually higher, but when taking into consideration the high cost of health care bills it may be some sort of a safer route to take to protect your current financial potential.

I’ve to say you’ve been really helpful to me. Thank you!

Your articles are incredibly helpful to me. Thank you! May I request more information?

I have realized that of all types of insurance, health insurance is the most dubious because of the issue between the insurance company’s need to remain profitable and the consumer’s need to have insurance plan. Insurance companies’ profits on health and fitness plans are certainly low, consequently some providers struggle to generate income. Thanks for the concepts you reveal through this website.

Thank you for your help. I must say you’ve been really helpful to me.

Thank you for the sensible critique. Me & my neighbor were just preparing to do some research about this. We got a grab a book from our local library but I think I learned more from this post. I am very glad to see such magnificent info being shared freely out there.

Great blog post. What I would like to bring about is that computer memory has to be purchased when your computer still can’t cope with what you do along with it. One can put in two RAM memory boards having 1GB each, for example, but not certainly one of 1GB and one having 2GB. One should make sure the car maker’s documentation for the PC to ensure what type of ram is necessary.

You’ve been great to me. Thank you!

May I request that you elaborate on that? Your posts have been extremely helpful to me. Thank you!

Please provide me with additional details on that. I need to learn more about it.

СамоИрония судьбы смотреть

Thanks for the recommendations shared on your blog. Another thing I would like to express is that fat reduction is not information about going on a dietary fads and trying to shed as much weight as possible in a couple of days. The most effective way to shed pounds is by consuming it bit by bit and using some basic points which can allow you to make the most from a attempt to shed pounds. You may learn and be following many of these tips, although reinforcing expertise never affects.

Thanks for the tips shared using your blog. One more thing I would like to say is that weight-loss is not information about going on a fad diet and trying to shed as much weight as you’re able in a set period of time. The most effective way in losing weight is by having it gradually and obeying some basic suggestions which can help you to make the most through your attempt to slim down. You may realize and already be following some tips, but reinforcing awareness never damages.

One other issue is that if you are in a circumstance where you don’t have a co-signer then you may want to try to wear out all of your financial aid options. You could find many grants and other scholarships that will present you with finances to help you with college expenses. Thanks alot : ) for the post.

It was really helpful to read an article like this one, because it helped me learn about the topic.

Dude these articles are amazing. They helped me a lot.

Just wish to say your article is as surprising. The clarity in your post is simply great and i can assume you’re an expert on this subject. Well with your permission allow me to grab your feed to keep updated with forthcoming post. Thanks a million and please keep up the rewarding work.

It was really helpful to read an article like this one, because it helped me learn about the topic.

Your articles are incredibly helpful to me. Thank you! May I request more information?

Your articles are extremely helpful to me. May I ask for more information?

Dude these articles have been really helpful to me. They really helped me out.

Thank you for being of assistance to me. I really loved this article.

May I request that you elaborate on that? Your posts have been extremely helpful to me. Thank you!

I was recommended this website by my cousin. I’m not sure whether this post is written by him as no one else know such detailed about my difficulty. You are wonderful! Thanks!

Thank you for posting this post. I found it extremely helpful because it explained what I was trying to say. I hope it can help others as well.

Thank you for writing the article. I like the topic too.

Wow! This can be one particular of the most useful blogs We’ve ever arrive across on this subject. Actually Wonderful. I am also a specialist in this topic so I can understand your effort.

Thanks a lot for the helpful posting. It is also my belief that mesothelioma cancer has an particularly long latency time, which means that warning signs of the disease might not emerge until 30 to 50 years after the first exposure to asbestos. Pleural mesothelioma, that’s the most common form and influences the area around the lungs, could cause shortness of breath, chest pains, as well as a persistent cough, which may bring on coughing up maintain.

I really enjoyed reading your post and it helped me a lot

I’ve to say you’ve been really helpful to me. Thank you!

Thanks for your help and for posting this. It’s been great.

It would be nice to know more about that. Your articles have always been helpful to me. Thank you!

Thank you for writing such a great article. It helped me a lot and I love the subject.

We’re a gaggle of volunteers and starting a brand new scheme in our community. Your website offered us with valuable information to paintings on. You’ve performed a formidable task and our entire group can be grateful to you.

I was suggested this website by my cousin. I’m not sure whether this post is written by him as no one else know such detailed about my difficulty. You’re wonderful! Thanks!

I do believe all of the concepts you have introduced to your post. They’re very convincing and will definitely work. Still, the posts are very short for newbies. Could you please extend them a little from next time? Thanks for the post.

Youre so cool! I dont suppose Ive learn something like this before. So good to find someone with some original ideas on this subject. realy thank you for starting this up. this web site is one thing that is needed on the web, somebody with just a little originality. helpful job for bringing something new to the internet!

One more thing is that when looking for a good on the net electronics retail outlet, look for online stores that are regularly updated, keeping up-to-date with the most recent products, the most effective deals, and helpful information on products and services. This will make certain you are doing business with a shop that stays on top of the competition and provides you what you ought to make educated, well-informed electronics buying. Thanks for the critical tips I have learned from your blog.

You can certainly see your enthusiasm in the work you write. The sector hopes for more passionate writers like you who are not afraid to say how they believe. All the time follow your heart.

Thanks for the good writeup. It actually was a enjoyment account it. Glance complicated to far delivered agreeable from you! However, how can we communicate?

I have recently started a site, the information you provide on this site has helped me greatly. Thanks for all of your time & work.

Thanks for your article. My partner and i have constantly seen that the majority of people are desirous to lose weight simply because wish to look slim and also attractive. Nonetheless, they do not continually realize that there are other benefits for losing weight also. Doctors assert that obese people come across a variety of illnesses that can be directly attributed to the excess weight. Thankfully that people that are overweight in addition to suffering from numerous diseases are able to reduce the severity of their illnesses through losing weight. You’ll be able to see a continuous but noted improvement with health when even a minor amount of weight reduction is realized.

Good post. I be taught something tougher on completely different blogs everyday. It’ll always be stimulating to read content material from other writers and apply a little bit something from their store. I?d desire to make use of some with the content material on my weblog whether you don?t mind. Natually I?ll provide you with a hyperlink in your web blog. Thanks for sharing.

I like the valuable info you provide in your articles. I?ll bookmark your weblog and check again here frequently. I am quite certain I?ll learn many new stuff right here! Good luck for the next!

I’ve recently started a blog, the information you provide on this website has helped me greatly. Thanks for all of your time & work.

Hmm it looks like your blog ate my first comment (it was extremely long) so I guess I’ll just sum it up what I had written and say, I’m thoroughly enjoying your blog. I too am an aspiring blog blogger but I’m still new to everything. Do you have any tips for rookie blog writers? I’d definitely appreciate it.

I have been browsing online more than 3 hours today, yet I never found any interesting article like yours. It?s pretty worth enough for me. In my view, if all site owners and bloggers made good content as you did, the net will be a lot more useful than ever before.

I have observed that car insurance firms know the motors which are vulnerable to accidents along with risks. Additionally they know what form of cars are prone to higher risk as well as higher risk they have the higher a premium price. Understanding the uncomplicated basics with car insurance can help you choose the right form of insurance policy that could take care of your preferences in case you become involved in an accident. Thank you sharing your ideas in your blog.

It is really a great and useful piece of information. I?m glad that you shared this useful info with us. Please keep us up to date like this. Thank you for sharing.

Hi there, just became aware of your blog through Google, and found that it is truly informative. I?m going to watch out for brussels. I?ll appreciate if you continue this in future. Lots of people will be benefited from your writing. Cheers!

I am not sure where you are getting your information, but great topic. I needs to spend some time learning much more or understanding more. Thanks for fantastic info I was looking for this information for my mission.

Thanks for your write-up. Another item is that being a photographer entails not only problem in capturing award-winning photographs but additionally hardships in establishing the best video camera suited to your requirements and most especially hardships in maintaining the standard of your camera. This is very genuine and obvious for those photographers that are in capturing a nature’s captivating scenes – the mountains, the forests, the particular wild or the seas. Going to these adventurous places certainly requires a camera that can meet the wild’s nasty environments.

Thanks for the posting. I have always seen that almost all people are wanting to lose weight as they wish to appear slim plus attractive. Nevertheless, they do not often realize that there are other benefits to losing weight also. Doctors insist that over weight people are afflicted with a variety of conditions that can be directly attributed to the excess weight. The good thing is that people who sadly are overweight along with suffering from numerous diseases can help to eliminate the severity of the illnesses simply by losing weight. You’ll be able to see a gradual but marked improvement in health if even a slight amount of weight reduction is accomplished.

I’ve observed that in the world nowadays, video games are the latest fad with children of all ages. There are times when it may be not possible to drag your son or daughter away from the video games. If you want the very best of both worlds, there are several educational activities for kids. Interesting post.

I think this is among the most vital info for me. And i’m glad reading your article. But should remark on few general things, The web site style is wonderful, the articles is really nice : D. Good job, cheers

Today, with the fast way of life that everyone is having, credit cards have a huge demand throughout the market. Persons out of every field are using the credit card and people who not using the card have prepared to apply for just one. Thanks for giving your ideas on credit cards.

Thanks for your post on the traveling industry. We would also like to include that if you’re a senior thinking about traveling, it is absolutely imperative that you buy traveling insurance for elderly people. When traveling, seniors are at greatest risk being in need of a health-related emergency. Receiving the right insurance policies package for the age group can safeguard your health and provide you with peace of mind.

I have seen a great deal of useful points on your internet site about desktops. However, I have the impression that notebook computers are still not nearly powerful sufficiently to be a good selection if you often do jobs that require loads of power, including video modifying. But for website surfing, statement processing, and many other prevalent computer work they are all right, provided you can’t mind the tiny screen size. Thank you for sharing your opinions.

With almost everything which seems to be building within this subject material, your viewpoints are generally rather stimulating. On the other hand, I appologize, because I do not give credence to your entire strategy, all be it radical none the less. It looks to everybody that your opinions are not totally justified and in reality you are yourself not even totally certain of your point. In any event I did enjoy looking at it.

Great work! This is the type of info that should be shared around the net. Shame on Google for not positioning this post higher! Come on over and visit my website . Thanks =)

Hentai

hentaihavenxxx.ru

гдз по русскому языку второй класс

гдз алгебра 8 класс колягин

I truly love your blog.. Very nice colors & theme. Did you make this web site yourself? Please reply back as I’m planning to create my own blog and would love to learn where you got this from or just what the theme is named. Many thanks.

After looking into a number of the blog posts on your blog, I seriously like your technique of blogging. I saved it to my bookmark site list and will be checking back soon. Take a look at my web site as well and tell me your opinion.

Saved as a favorite, I like your website.

Thank you for every other excellent article. Where else could anybody get that kind of info in such an ideal approach of writing? I have a presentation subsequent week, and I’m at the look for such information.

Hello my loved one! I wish to say that this post is awesome, great written and come with approximately all important infos. I would like to see more posts like this .

Thanks for discussing your ideas. One thing is that pupils have an option between fed student loan and a private education loan where it truly is easier to go with student loan debt consolidation than over the federal education loan.

I have seen loads of useful things on your web page about pcs. However, I’ve got the viewpoint that notebooks are still more or less not powerful adequately to be a good option if you normally do projects that require loads of power, such as video editing and enhancing. But for world-wide-web surfing, statement processing, and the majority of other typical computer work they are fine, provided you don’t mind the small screen size. Appreciate sharing your notions.

контурная карта 7 класс

гдз по английскому 9 класс starlight

967 оператор

гдз английский язык 5 класс

гдз по немецкому 6 класс

гдз по английскому 9 класс афанасьева

гдз по математике 4 класс дорофеев миракова бука

гдз по русскому 4класс

впр по истории 7 класс

гдз математика 5 класс виленкин

гдз по географии 7 класс

морфологический разбор прилагательного

гдз по английскому 10 класс вербицкая

гдз по русскому языку 5 класс быстрова

One thing I have actually noticed is the fact that there are plenty of common myths regarding the banking institutions intentions if talking about home foreclosure. One fantasy in particular would be the fact the bank desires your house. Your banker wants your dollars, not your own home. They want the amount of money they gave you together with interest. Avoiding the bank will draw a new foreclosed realization. Thanks for your post.

One more important component is that if you are an elderly person, travel insurance with regard to pensioners is something you should make sure you really consider. The mature you are, a lot more at risk you might be for permitting something undesirable happen to you while in foreign countries. If you are definitely not covered by many comprehensive insurance policy, you could have a number of serious difficulties. Thanks for giving your good tips on this web blog.

After exploring a few of the articles on your website, I really like your technique of blogging. I saved as a favorite it to my bookmark site list and will be checking back soon. Please visit my web site too and tell me what you think.

Your style is really unique in comparison to other folks I’ve read stuff from. Thank you for posting when you have the opportunity, Guess I will just book mark this site.

I was very pleased to discover this web site. I need to to thank you for your time due to this wonderful read!! I definitely loved every little bit of it and i also have you bookmarked to check out new information in your site.

With the whole thing that appears to be building inside this specific area, a significant percentage of perspectives tend to be rather refreshing. Nevertheless, I appologize, but I can not subscribe to your entire idea, all be it radical none the less. It looks to everyone that your comments are generally not completely rationalized and in actuality you are your self not even totally convinced of the point. In any event I did enjoy looking at it.

Great site. A lot of useful info here. I?m sending it to some friends ans also sharing in delicious. And certainly, thanks for your effort!

I?m not sure where you’re getting your information, but great topic. I needs to spend some time learning much more or understanding more. Thanks for magnificent information I was looking for this info for my mission.

I was just searching for this info for a while. After six hours of continuous Googleing, finally I got it in your web site. I wonder what is the lack of Google strategy that do not rank this type of informative web sites in top of the list. Generally the top sites are full of garbage.

Hello there, You have done a fantastic job. I will definitely digg it and individually suggest to my friends. I’m confident they’ll be benefited from this website.

I used to be more than happy to seek out this net-site.I wished to thanks to your time for this glorious learn!! I undoubtedly enjoying every little bit of it and I have you bookmarked to take a look at new stuff you blog post.

9xflix dum laga ke haisha

That is really interesting, You’re a very skilled blogger. I have joined your rss feed and look ahead to in search of more of your wonderful post. Also, I have shared your website in my social networks!

9xflix movie download 2022

hindi dubbed-9xflix

Heya i am for the primary time here. I came across this board and I in finding It truly useful & it helped me out much. I’m hoping to offer something back and help others like you aided me.

Excellent website. Plenty of useful info here. I?m sending it to a few friends ans also sharing in delicious. And certainly, thanks for your effort!

Heya i?m for the primary time here. I came across this board and I in finding It truly helpful & it helped me out a lot. I’m hoping to give something again and aid others like you aided me.

xanxx

This website online is really a walk-through for all of the data you wished about this and didn?t know who to ask. Glimpse right here, and also you?ll undoubtedly uncover it.

I have not checked in here for some time since I thought it was getting boring, but the last several posts are good quality so I guess I will add you back to my everyday bloglist. You deserve it my friend 🙂

movies free inline

obviously like your website but you need to take a look at the spelling on quite a few of your posts. A number of them are rife with spelling problems and I in finding it very bothersome to tell the truth however I will certainly come again again.

I really appreciate this post. I have been looking everywhere for this! Thank goodness I found it on Bing. You’ve made my day! Thank you again

Great post right here. One thing I would really like to say is the fact most professional job areas consider the Bachelors Degree like thejust like the entry level standard for an online diploma. When Associate College diplomas are a great way to get started, completing the Bachelors presents you with many good opportunities to various employment goodies, there are numerous on-line Bachelor Course Programs available from institutions like The University of Phoenix, Intercontinental University Online and Kaplan. Another issue is that many brick and mortar institutions present Online variants of their college diplomas but often for a considerably higher cost than the companies that specialize in online diploma plans.

One thing I would really like to say is the fact that car insurance termination is a horrible experience and if you are doing the proper things as being a driver you’ll not get one. A number of people do have the notice that they are officially dumped by their particular insurance company they then have to struggle to get additional insurance after a cancellation. Low cost auto insurance rates usually are hard to get from cancellation. Understanding the main reasons pertaining to auto insurance cancellations can help people prevent completely losing in one of the most critical privileges accessible. Thanks for the strategies shared by means of your blog.

This actually answered my drawback, thank you!

Hello, i feel that i saw you visited my site so i came to ?return the prefer?.I am attempting to find issues to improve my website!I assume its ok to make use of a few of your ideas!!

Undeniably believe that that you stated. Your favorite justification seemed to be at the net the simplest factor to have in mind of. I say to you, I definitely get irked while other folks consider concerns that they plainly do not realize about. You controlled to hit the nail upon the highest and also defined out the entire thing without having side effect , people could take a signal. Will probably be again to get more. Thank you

I get pleasure from, result in I found exactly what I was having a look for. You’ve ended my four day long hunt! God Bless you man. Have a nice day. Bye

I have noticed that fixing credit activity really needs to be conducted with techniques. If not, you are going to find yourself damaging your rating. In order to reach your goals in fixing your credit history you have to see to it that from this minute you pay all of your monthly dues promptly in advance of their appointed date. Really it is significant because by not really accomplishing that, all other steps that you will choose to use to improve your credit rank will not be successful. Thanks for discussing your strategies.

I was able to find good info from your blog articles.

I like looking through a post that will make men and women think. Also, thank you for allowing for me to comment.

You could definitely see your expertise in the work you write. The world hopes for even more passionate writers like you who are not afraid to say how they believe. Always follow your heart.

Thanks for the suggestions you are sharing on this website. Another thing I’d like to say is getting hold of some copies of your credit report in order to check accuracy of the detail is one first step you have to accomplish in credit restoration. You are looking to thoroughly clean your credit file from harmful details problems that screw up your credit score.

I have noticed that over the course of making a relationship with real estate proprietors, you’ll be able to come to understand that, in every real estate purchase, a fee is paid. In the end, FSBO sellers tend not to “save” the fee. Rather, they try to earn the commission by way of doing a great agent’s job. In doing this, they expend their money and time to conduct, as best they will, the tasks of an representative. Those duties include uncovering the home via marketing, showing the home to buyers, making a sense of buyer emergency in order to prompt an offer, organizing home inspections, handling qualification inspections with the mortgage lender, supervising maintenance, and assisting the closing of the deal.

The core of your writing whilst sounding reasonable initially, did not settle very well with me personally after some time. Someplace throughout the paragraphs you actually were able to make me a believer but just for a short while. I still have a problem with your jumps in logic and you would do well to help fill in those breaks. In the event you can accomplish that, I would certainly be impressed.

Thanks , I have recently been searching for information about this subject for ages and yours is the best I have discovered so far. But, what about the bottom line? Are you sure about the source?

Thanks for your fascinating article. Other thing is that mesothelioma is generally a result of the breathing of fibres from asbestos fiber, which is a cancer causing material. It’s commonly viewed among laborers in the engineering industry who may have long exposure to asbestos. It is also caused by moving into asbestos insulated buildings for some time of time, Genes plays a crucial role, and some persons are more vulnerable towards the risk in comparison with others.

Thanks for your valuable post. In recent times, I have been able to understand that the actual symptoms of mesothelioma are caused by your build up associated fluid involving the lining of your lung and the chest cavity. The sickness may start within the chest area and multiply to other body parts. Other symptoms of pleural mesothelioma cancer include fat loss, severe respiration trouble, a fever, difficulty taking in food, and inflammation of the neck and face areas. It really should be noted that some people existing with the disease tend not to experience virtually any serious signs and symptoms at all.

I could not resist commenting. Well written.

Hello there! This blog post couldn’t be written any better! Going through this post reminds me of my previous roommate! He continually kept talking about this. I’ll forward this article to him. Pretty sure he will have a great read. Many thanks for sharing!

Way cool! Some extremely valid points! I appreciate you writing this article and also the rest of the site is also very good.

Wow, superb blog format! How lengthy have you been running a blog for? you make blogging look easy. The entire look of your web site is wonderful, as neatly as the content material!

I’ve observed that in the world the present day, video games are classified as the latest fad with children of all ages. There are occassions when it may be extremely hard to drag your son or daughter away from the games. If you want the very best of both worlds, there are many educational video games for kids. Great post.

I’ve come across that these days, more and more people are attracted to camcorders and the industry of images. However, to be a photographer, you have to first spend so much time frame deciding which model of digicam to buy and moving from store to store just so you might buy the least expensive camera of the trademark you have decided to select. But it won’t end just there. You also have take into consideration whether you should buy a digital photographic camera extended warranty. Thanks a lot for the good points I obtained from your website.

Excellent post. I was checking continuously this blog and I’m impressed! Extremely helpful info specifically the last part 🙂 I care for such info much. I was looking for this particular information for a long time. Thank you and best of luck.

Great website. A lot of useful information here. I am sending it to a few friends ans also sharing in delicious. And certainly, thanks for your sweat!

Thank you a lot for sharing this with all people you really know what you’re talking approximately! Bookmarked. Please also consult with my web site =). We will have a link exchange agreement between us!

Good site you have got here.. It’s difficult to find quality writing like yours these days. I truly appreciate individuals like you! Take care!!

One thing I’d like to say is the fact that car insurance cancellations is a terrifying experience so if you’re doing the correct things being a driver you simply will not get one. Many people do obtain notice that they are officially dumped by the insurance company and several have to fight to get additional insurance after the cancellation. Inexpensive auto insurance rates are generally hard to get from a cancellation. Having the main reasons with regard to auto insurance cancellation can help people prevent getting rid of in one of the most crucial privileges available. Thanks for the strategies shared through your blog.

Howdy! This post couldn’t be written any better! Looking through this post reminds me of my previous roommate! He always kept talking about this. I am going to send this post to him. Fairly certain he’ll have a very good read. I appreciate you for sharing!

Hi there, I found your blog via Google while searching for a related topic, your website came up, it looks good. I have bookmarked it in my google bookmarks.

Good post here. One thing I would really like to say is the fact that most professional career fields consider the Bachelor’s Degree just as the entry level standard for an online course. Even though Associate Degrees are a great way to get started, completing your own Bachelors reveals many good opportunities to various employment opportunities, there are numerous internet Bachelor Diploma Programs available via institutions like The University of Phoenix, Intercontinental University Online and Kaplan. Another thing is that many brick and mortar institutions make available Online editions of their diplomas but commonly for a drastically higher charge than the companies that specialize in online degree programs.

Great site. Lots of useful information here. I am sending it to several pals ans also sharing in delicious. And certainly, thank you for your effort!

Thanks for the suggestions you are giving on this web site. Another thing I would like to say is getting hold of duplicates of your credit history in order to check out accuracy of each detail is the first action you have to carry out in fixing credit. You are looking to thoroughly clean your credit history from dangerous details flaws that screw up your credit score.

When I initially commented I clicked the -Notify me when new feedback are added- checkbox and now every time a comment is added I get 4 emails with the same comment. Is there any manner you can take away me from that service? Thanks!

Aw, this was a really nice post. In concept I want to put in writing like this moreover ? taking time and actual effort to make an excellent article? however what can I say? I procrastinate alot and by no means seem to get something done.

Hi, i think that i saw you visited my site thus i came to ?return the favor?.I am attempting to find things to improve my web site!I suppose its ok to use some of your ideas!!

I will immediately grab your rss as I can’t find your email subscription link or e-newsletter service. Do you have any? Please let me know so that I could subscribe. Thanks.

Thanks a lot for the helpful write-up. It is also my belief that mesothelioma cancer has an really long latency time, which means that signs and symptoms of the disease might not exactly emerge until eventually 30 to 50 years after the original exposure to asbestos. Pleural mesothelioma, which can be the most common sort and impacts the area within the lungs, could potentially cause shortness of breath, chest pains, as well as a persistent coughing, which may cause coughing up blood.

Undeniably believe that which you stated. Your favorite justification appeared to be on the net the easiest thing to be aware of. I say to you, I certainly get irked while people think about worries that they just don’t know about. You managed to hit the nail upon the top and also defined out the whole thing without having side-effects , people could take a signal. Will probably be back to get more. Thanks

Thanks for your publication. I would also love to say that the first thing you will need to complete is determine whether you really need repairing credit. To do that you need to get your hands on a copy of your credit score. That should really not be difficult, ever since the government mandates that you are allowed to receive one free of charge copy of your actual credit report per year. You just have to check with the right men and women. You can either look at website owned by the Federal Trade Commission or perhaps contact one of the main credit agencies immediately.

I do not even know how I ended up here, but I thought this post was great. I do not know who you are but certainly you’re going to a famous blogger if you aren’t already 😉 Cheers!

Hello there! I could have sworn I’ve been to this web site before but after looking at some of the articles I realized it’s new to me. Anyways, I’m certainly happy I discovered it and I’ll be bookmarking it and checking back often!

We are a group of volunteers and opening a new scheme in our community. Your web site provided us with valuable info to work on. You’ve done a formidable job and our entire community will be thankful to you.

Someone necessarily assist to make critically posts I would state. That is the very first time I frequented your web page and up to now? I surprised with the research you made to make this particular post extraordinary. Fantastic activity!

Thank you for the auspicious writeup. It in fact was a amusement account it. Look advanced to far added agreeable from you! However, how can we communicate?

Great goods from you, man. I have take note your stuff prior to and you are simply too wonderful. I actually like what you have obtained right here, really like what you’re saying and the way in which through which you assert it. You are making it enjoyable and you continue to take care of to keep it sensible. I can’t wait to learn far more from you. That is actually a great site.

Nice post. I was checking constantly this blog and I’m impressed! Very useful information specifically the last part 🙂 I care for such information much. I was seeking this certain information for a long time. Thank you and best of luck.

I love reading through an article that can make people think. Also, thank you for allowing me to comment.

Excellent article! We are linking to this great post on our website. Keep up the great writing.

After I initially commented I seem to have clicked the -Notify me when new comments are added- checkbox and now each time a comment is added I get 4 emails with the same comment. There has to be a way you are able to remove me from that service? Appreciate it.

Thanks for your article. One other thing is individual states in the United states of america have their unique laws that affect house owners, which makes it extremely tough for the the legislature to come up with the latest set of recommendations concerning property foreclosure on householders. The problem is that every state has own regulations which may interact in a negative manner in regards to foreclosure insurance policies.

Thanks for your post. One other thing is that often individual states in the United states of america have their unique laws of which affect home owners, which makes it extremely tough for the our elected representatives to come up with a fresh set of rules concerning home foreclosure on homeowners. The problem is that a state has got own guidelines which may have interaction in a damaging manner on the subject of foreclosure insurance plans.

Pretty! This was an extremely wonderful article. Thank you for providing these details.

I think this is one of the most significant info for me. And i’m glad reading your article. But wanna remark on some general things, The web site style is wonderful, the articles is really nice : D. Good job, cheers

Thank you, I’ve just been looking for information approximately this topic for a long time and yours is the greatest I have came upon till now. But, what in regards to the bottom line? Are you sure concerning the supply?

I was just seeking this information for some time. After six hours of continuous Googleing, finally I got it in your site. I wonder what’s the lack of Google strategy that don’t rank this type of informative web sites in top of the list. Generally the top web sites are full of garbage.

This website was… how do you say it? Relevant!! Finally I have found something that helped me. Kudos.

Thanks for some other informative site. Where else may just I get that type of information written in such an ideal means? I have a project that I’m just now running on, and I’ve been on the look out for such information.

Thank you sharing these types of wonderful blogposts. In addition, the ideal travel along with medical insurance approach can often reduce those considerations that come with visiting abroad. Your medical crisis can shortly become expensive and that’s sure to quickly decide to put a financial burden on the family’s finances. Putting in place the suitable travel insurance deal prior to setting off is well worth the time and effort. Thanks

I was more than happy to seek out this internet-site.I wanted to thanks on your time for this wonderful learn!! I undoubtedly having fun with every little little bit of it and I’ve you bookmarked to take a look at new stuff you blog post.

hi!,I really like your writing very much! share we keep in touch extra about your post on AOL? I require an expert on this house to resolve my problem. May be that’s you! Taking a look forward to look you.

Hello There. I discovered your blog the use of msn. That is a very well written article. I will make sure to bookmark it and come back to read extra of your helpful information. Thank you for the post. I?ll certainly comeback.

You ought to be a part of a contest for one of the best blogs on the net. I will highly recommend this web site!

I was able to find good info from your blog posts.

This is a topic that is close to my heart… Cheers! Where are your contact details though?

Hello, Neat post. There is a problem together with your website in internet explorer, may check this? IE still is the marketplace chief and a good element of other people will pass over your great writing because of this problem.

Real clean website , thankyou for this post.

My brother suggested I might like this website. He was totally right. This post actually made my day. You cann’t imagine just how much time I had spent for this info! Thanks!