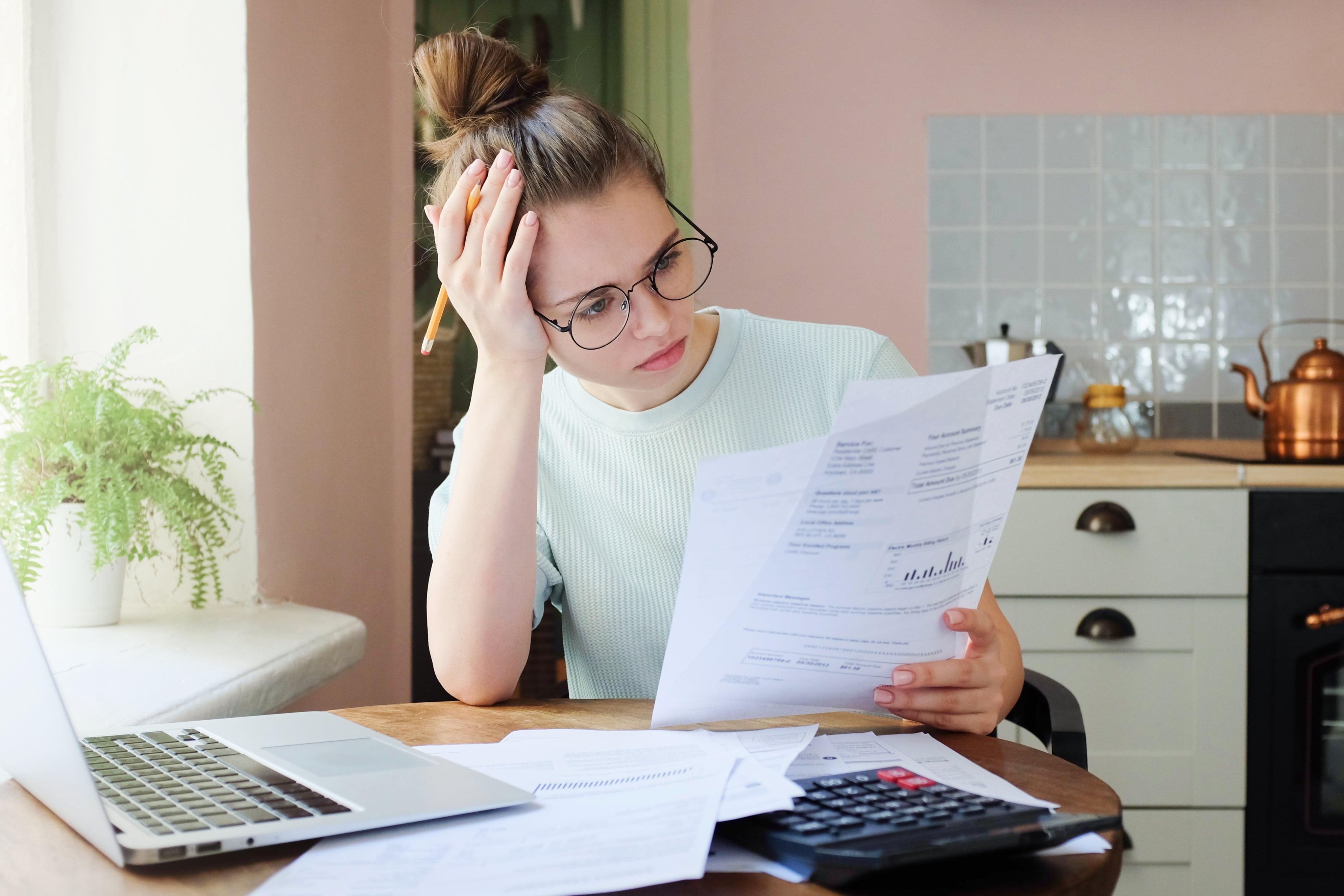

The vast majority of Americans carry some level of debt. When financial pressures are high, you may be searching for relief options. Due to the stigma attached to bankruptcy, a debt consolidation loan is a tempting alternative. Debt consolidation loans combine your existing debts into one payment, making it a bit easier to manage your payment and reducing your interest rate.

Debt Consolidation Options

There are two kinds of debt consolidation loans. One requires the use of your home as collateral. This option can put your home at risk. However, if you eventually need to file for Chapter 7 bankruptcy, this form of debt consolidation reduces the amount of equity you have in your home, increasing the chance that you will be able to keep your home under Georgia’s exemptions. These legal exemptions allow for $21,500 in home equity or double that if you are married.

Another option is an unsecured debt consolidation, which does not require collateral. Instead, this form of debt consolidation pays off all of your existing creditors in exchange for one new loan.

Both options typically offer a lower interest rate. The lower interest rate and, often, longer repayment term results in lower monthly payments. However, the low-interest rate is sometimes just a temporary, introductory rate, so read the fine print carefully.

Consolidation Considerations

Before you agree to a debt consolidation loan, make sure you do your homework. Although debt consolidation companies are governed by Georgia’s Debt Adjustment Act, which limits the fees allowed to be collected and requires certain business practices, this does not mean that debt consolidation is always advantageous for you. The interest rate, fees, and repayment term may create a greater financial burden for you than the original loans. Make sure that you do the math to determine:

- The full amount you will repay in your current loan payment plans

- The full amount you will pay with the proposed debt consolidation loan

- Your ability to meet the monthly payments required under both options

If the consolidation will increase the amount you pay over time, it would be wise to seek other options. Similarly, you should not commit to a debt consolidation loan that you know you cannot pay each month.

When it is Time for a Debt Consolidation Loan

Once you have considered all of the above, you are closer to determining whether or not a debt consolidation loan is for you. In particular, debt consolidation might be for you if:

- You have extremely high-interest rate debts

- You qualify for a very low-interest rate loan

- You have the income needed to make payments

- You have a plan to remain out of debt once your loan is paid off

If you will not be able to pay off the debt consolidation loan or otherwise do not meet the qualities listed above, you will want to explore other options that may be more suitable for your situation.

Contact an Attorney Today

Before you make any decisions about managing your debt or engage in debt consolidation loans, contact the experienced attorneys at Cornwell Law Firm. We will help you to determine the best option for dealing with your debt, even if it is not declaring bankruptcy.

… [Trackback]

[…] Read More here to that Topic: cornwellbankruptcy.com/advice/debt-consolidation-loans/ […]

… [Trackback]

[…] Read More on on that Topic: cornwellbankruptcy.com/advice/debt-consolidation-loans/ […]

… [Trackback]

[…] Information on that Topic: cornwellbankruptcy.com/advice/debt-consolidation-loans/ […]

http://6600lonetree.com/betchain-casino-no-deposit-bonus-codes-casino-dice-bulk/

https://chaali.com/africa/the-sars-commissioner-will-set-more-than-5-million-repayments-within-the-deadline/

Hi to every body, it’s my first visit of this blog; this blog carries amazing and in fact excellent information in favor of readers.|

For latest information you have to pay a quick visit world wide web and on world-wide-web I found this web site as a most excellent site for newest updates.|

Excellent blog you have here.. It’s hard to find excellent writing like yours nowadays. I really appreciate individuals like you! Take care!!|

Heya! I’m at work browsing your blog from my new iphone 3gs! Just wanted to say I love reading your blog and look forward to all your posts! Keep up the outstanding work!|

Hello would you mind letting me know which webhost you’re working with? I’ve loaded your blog in 3 completely different web browsers and I must say this blog loads a lot quicker then most. Can you recommend a good internet hosting provider at a fair price? Thanks a lot, I appreciate it!|

Hi there! I just wanted to ask if you ever have any issues with hackers? My last blog (wordpress) was hacked and I ended up losing many months of hard work due to no data backup. Do you have any methods to protect against hackers?|

Please let me know if you’re looking for a writer for your site. You have some really great articles and I think I would be a good asset. If you ever want to take some of the load off, I’d absolutely love to write some material for your blog in exchange for a link back to mine. Please blast me an email if interested. Thanks!|

Hi to every one, because I am really eager of reading this web site’s post to be updated on a regular basis. It consists of good material.|

… [Trackback]

[…] Find More here to that Topic: cornwellbankruptcy.com/advice/debt-consolidation-loans/ […]

Hi my loved one! I wish to say that this article is amazing, great written and come with almost all significant infos. I’d like to see more posts like this .|

Keep on writing, great job!|

This is very interesting, You are a very skilled blogger. I have joined your rss feed and look forward to seeking more of your excellent post. Also, I’ve shared your website in my social networks!

These are genuinely fantastic ideas in on the topic of blogging. You have touched some pleasant factors here. Any way keep up wrinting.|

… [Trackback]

[…] Info to that Topic: cornwellbankruptcy.com/advice/debt-consolidation-loans/ […]

I’m impressed, I have to admit. Seldom do I encounter a blog that’s equally educative and engaging, and let me tell you, you’ve hit the nail on the head. The issue is something too few people are speaking intelligently about. I’m very happy I found this in my search for something regarding this.|

… [Trackback]

[…] Here you will find 90965 more Info to that Topic: cornwellbankruptcy.com/advice/debt-consolidation-loans/ […]

… [Trackback]

[…] Information to that Topic: cornwellbankruptcy.com/advice/debt-consolidation-loans/ […]

Regards for helping out, superb info .

I think this is one of the most vital information for me. And i am glad reading your article. But should remark on some general things, The site style is great, the articles is really great : D. Good job, cheers|

Its like you read my mind! You seem to know a lot about this, like you wrote the book in it or something. I think that you could do with a few pics to drive the message home a little bit, but instead of that, this is fantastic blog. A fantastic read. I’ll certainly be back.|

Pretty! This was a really wonderful article. Thanks for providing this information.|

I’m really impressed with your writing skills as well as with the layout on your blog. Is this a paid theme or did you modify it yourself? Either way keep up the excellent quality writing, it is rare to see a great blog like this one today.|

… [Trackback]

[…] Read More Info here on that Topic: cornwellbankruptcy.com/advice/debt-consolidation-loans/ […]

Valuable info. Fortunate me I found your website unintentionally, and I am shocked why this coincidence did not took place in advance! I bookmarked it.

Hi there, just wanted to say, I liked this post. It was practical. Keep on posting!|

Hi there would you mind sharing which blog platform you’re using? I’m going to start my own blog in the near future but I’m having a difficult time making a decision between BlogEngine/Wordpress/B2evolution and Drupal. The reason I ask is because your layout seems different then most blogs and I’m looking for something unique. P.S Sorry for getting off-topic but I had to ask!|

Good article! We are linking to this great content on our website. Keep up the good writing.|

Thanks-a-mundo for the article.Thanks Again. Really Great.

Appreciate this post. Let me try it out.|

I go to see day-to-day a few web pages and websites to read articles or reviews, however this webpage provides quality based writing.|

No matter if some one searches for his essential thing, so he/she wishes to be available that in detail, thus that thing is maintained over here.|

Excellent web site you’ve got here.. It’s hard to find good quality writing like yours these days. I really appreciate individuals like you! Take care!!|

… [Trackback]

[…] Find More Information here to that Topic: cornwellbankruptcy.com/advice/debt-consolidation-loans/ […]

Nice post. I was checking constantly this blog and I’m impressed! Very useful information specially the last part 🙂 I care for such info much. I was looking for this certain information for a long time. Thank you and good luck.|

Good day! This is my first comment here so I just wanted to give a quick shout out and tell you I genuinely enjoy reading through your articles. Can you suggest any other blogs/websites/forums that go over the same topics? Appreciate it!|

There’s certainly a great deal to learn about this subject. I really like all of the points you have made.|

Have you ever thought about including a little bit more than just your articles? I mean, what you say is valuable and all. But think of if you added some great images or video clips to give your posts more, “pop”! Your content is excellent but with pics and videos, this blog could certainly be one of the greatest in its field. Awesome blog!|

… [Trackback]

[…] Here you will find 51027 more Information on that Topic: cornwellbankruptcy.com/advice/debt-consolidation-loans/ […]

I blog frequently and I really thank you for your content. Your article has truly peaked my interest. I am going to take a note of your website and keep checking for new information about once a week. I opted in for your RSS feed as well.|

Right now it looks like BlogEngine is the top blogging platform available right now. (from what I’ve read) Is that what you are using on your blog?|

My relatives all the time say that I am wasting my time here at net, however I know I am getting familiarity every day by reading such pleasant articles.|

Do you have a spam issue on this site; I also am a blogger, and I was wanting to know your situation; we have developed some nice practices and we are looking to swap techniques with others, be sure to shoot me an email if interested.|

You’re so cool! I don’t believe I’ve read something like that before. So great to discover another person with unique thoughts on this subject. Really.. thanks for starting this up. This site is something that’s needed on the internet, someone with some originality!|

Please let me know if you’re looking for a article author for your blog. You have some really good articles and I feel I would be a good asset. If you ever want to take some of the load off, I’d absolutely love to write some content for your blog in exchange for a link back to mine. Please blast me an e-mail if interested. Thanks!|

Simply desire to say your article is as astounding. The clarity in your publish is simply cool and that i could think you’re knowledgeable on this subject. Well with your permission let me to clutch your feed to keep up to date with coming near near post. Thanks 1,000,000 and please keep up the rewarding work.|

Hello how are you companions that garn press release 2020

Hi there! I could have sworn I’ve been to your blog before but after looking at some of the posts I realized it’s new to me. Anyways, I’m certainly pleased I stumbled upon it and I’ll be bookmarking it and checking back regularly!

Wow that was strange. I just wrote an extremely long comment but after I clicked submit my comment didn’t appear. Grrrr… well I’m not writing all that over again. Anyways, just wanted to say fantastic blog!|

We absolutely love your blog and find the majority of your post’s to be just what I’m looking for. Would you offer guest writers to write content available for you? I wouldn’t mind publishing a post or elaborating on many of the subjects you write about here. Again, awesome web log!|

I am regular visitor, how are you everybody? This article posted at this site is genuinely pleasant.|

I just could not go away your web site before suggesting that I really enjoyed the usual info a person supply on your guests? Is going to be back steadily in order to check out new posts|

Greate pieces. Keep writing such kind of information on your blog. Im really impressed by it.

What’s up, I check your blog regularly. Your story-telling style is witty, keep doing what you’re doing!|

This is a topic which is near to my heart… Many thanks! Where are your contact details though?|

Hi there, this weekend is good in favor of me, for the reason that this moment i am reading this enormous educational post here at my house.|

you are truly a good webmaster. The web site loading speed is incredible. It kind of feels that you’re doing any distinctive trick. Also, The contents are masterpiece. you have performed a wonderful process on this topic!|

2statutes

cam chat gay https://bjsgaychatroom.info/

drug friendly gay dating sites https://gaypridee.com/

free one on one gay sex chat on camera for masterbation https://gaytgpost.com/

chat canada gay https://gay-buddies.com/

gay dating websites for kids https://speedgaydate.com/

I’d have to examine with you here. Which is not one thing I usually do! I take pleasure in reading a post that may make folks think. Additionally, thanks for permitting me to comment!

porn slots https://2-free-slots.com/

what slots pay the most https://freeonlneslotmachine.com/

ruby slippers slots https://candylandslotmachine.com/

scatter slots girls https://pennyslotmachines.org/

slots lv https://slotmachinesworld.com/

Aw, this was an exceptionally good post. Spending some time and actual effort to create a very good articleÖ but what can I sayÖ I procrastinate a lot and don’t seem to get anything done.

Hi my family member! I wish to say that this article is amazing, nice written and include approximately all important infos. I’d like to see more posts like this .

bowser slots mario party 2 https://slotmachinesforum.net/

las vegas slots free play https://slot-machine-sale.com/

lucky slots 777 free play https://beat-slot-machines.com/

hack online slots https://download-slot-machines.com/

sexy girl slots https://411slotmachine.com/

multiclass spell slots 5e https://www-slotmachines.com/

slots garden casino https://slotmachinegameinfo.com/

phd dissertation writing https://buydissertationhelp.com/

Attractive section of content. I just stumbled upon your website and in accession capital to assert that I acquire in fact enjoyed account your blog posts. Anyway I will be subscribing to your augment and even I achievement you access consistently fast.

mla dissertation citation https://dissertationwriting-service.com/

liberty university dissertation handbook https://help-with-dissertations.com/

uf dissertation search https://mydissertationwritinghelp.com/

help dissertation https://dissertations-writing.org/

I read this piece of writing completely concerning the difference of

newest and previous technologies, it’s awesome article.

Hello there! I love your content, keep it up. You’re so good at it. Also check out my blog, I’m sharing some good content. okuryazarlık

Unquestionably believe that which you said. Your favorite justification appeared to be on the web the simplest thing to be aware of. I say to you, I definitely get irked while people think about worries that they just don’t know about. You managed to hit the nail upon the top and also defined out the whole thing without having side effect , people can take a signal. Will likely be back to get more. Thanks

Hi there! I love your content, keep doing it. You’re so good at it. Also check out my website, I’m posting some amazing stuff. google account recovery

Hi there! I love your post, keep it up. You’re really professional at what you’re doing. Also check out my website, I’m posting some good content. recover my google account

Hi there! I love your content, keep it going. You’re really professional at it. Also check out my blog, I’m posting some good content. forgot gmail password

Hey there! I love your post, keep sharing it. You’re so professional at it. Also check out my blog, I’m posting some amazing stuff. gmail recovery page

Hi there! I like your post, keep sharing it. You’re so good at it. Also check out my blog, I’m posting some amazing stuff. recover gmail account

Hey there! I love your article, keep it up. You’re so professional at it. Also check out my website, I’m posting some good stuff. free robux

Hi there! I love your post, keep it going. You’re really good at it. Also check out my blog, I’m sharing some good stuff. free robux app

Hello there! I love your article, keep it going. You’re really good at what you’re doing. Also check out my website, I’m sharing some good content. free robux website

Hello there! I love your article, keep it up. You’re so professional at it. Also check out my blog, I’m sharing some good content. roblox robux

Hi there! I love your content, keep sharing it. You’re so professional at what you’re doing. Also check out my website, I’m posting some amazing stuff. free robux generator

Hi there! I like your content, keep it up. You’re really good at it. Also check out my blog, I’m sharing some good stuff. free robux no human verification

Hey there! I like your post, keep it going. You’re so professional at it. Also check out my blog, I’m sharing some good content. roblox robux

Hey there! I like your article, keep it up. You’re really good at what you’re doing. Also check out my website, I’m posting some amazing content. okur yazarlik

Hi there! I love your post, keep it going. You’re so good at what you’re doing. Also check out my blog, I’m sharing some good content. dilin anlamı nedir

Hey there! I like your post, keep doing it. You’re really good at what you’re doing. Also check out my website, I’m sharing some amazing content. okur yazarlık

Hello there! I like your post, keep doing it. You’re really good at it. Also check out my website, I’m sharing some good content. okur yazarlık

Hello there! I like your article, keep doing it. You’re really professional at what you’re doing. Also check out my website, I’m sharing some good content. dil nedir

Hello there! I love your article, keep doing it. You’re really professional at it. Also check out my website, I’m posting some amazing content. dil nedir

Hey there! I love your content, keep sharing it. You’re so good at what you’re doing. Also check out my blog, I’m sharing some amazing content. dil nedir

Hey there! I like your content, keep it up. You’re so professional at it. Also check out my website, I’m sharing some amazing stuff. dil nedir

Enjoyed the post

Wow that was odd. I just wrote an incredibly long comment but after I clicked submit my comment didn’t show up. Grrrr… well I’m not writing all that over again. Anyhow, just wanted to say wonderful blog!|

Thanks for the tips you are sharing on this weblog. Another thing I’d prefer to say is always that getting hold of some copies of your credit report in order to examine accuracy of each and every detail will be the first step you have to carry out in credit restoration. You are looking to thoroughly clean your credit history from dangerous details errors that ruin your credit score.

Good web site you have here.. It’s difficult to find good quality writing like yours nowadays. I truly appreciate individuals like you! Take care!!

Private proxies and most readily useful prices: 50 discount, free proxies and promotions – only on DreamProxies.com

Great post

Great post

Great post

Another good post

Loved every word

Any similar content?

Any similar content?

Another good post

Im grateful for the blog post. Great.

Pleasure to read

Enjoyed the read

A motivating discussion is definitely worth comment.

People who speak this love language often equate gifts to your love and devotion. They often feel good when you do not forget to give them an anniversary gift.

I am constantly thought about this, thankyou for putting up.

Психолог онлайн. Консультация Когда необходим прием психолога? – 7915 врачей, 3472 отзывов.

смотреть сериалы тут

Spot on with this write-up, I actually believe that this site needs far more attention. I’ll probably be back again to read more, thanks for the info!|

Aw, this was an incredibly good post. Spending some time and actual effort to produce a top notch article… but what can I say… I procrastinate a whole lot and don’t seem to get nearly anything done.|

Admiring the dedication you put into your site and detailed information you present. It’s great to come across a blog every once in a while that isn’t the same out of date rehashed information. Great read! I’ve bookmarked your site and I’m adding your RSS feeds to my Google account.|

Thanks for a marvelous posting! I definitely enjoyed reading it, you may be a great author. I will remember to bookmark your blog and may come back from now on. I want to encourage continue your great work, have a nice evening!|

In fact when someone doesn’t understand then its up to other people that they will assist, so here it occurs.|

Hi there, its pleasant post about media print, we all be aware of media is a wonderful source of information.|

Howdy! I know this is kinda off topic however , I’d figured I’d ask. Would you be interested in exchanging links or maybe guest writing a blog article or vice-versa? My blog discusses a lot of the same subjects as yours and I believe we could greatly benefit from each other. If you’re interested feel free to shoot me an email. I look forward to hearing from you! Wonderful blog by the way!|

Hi my friend! I want to say that this post is awesome, nice written and include approximately all vital infos. I’d like to see more posts like this .|

Every weekend i used to go to see this web page, for the reason that i want enjoyment, for the reason that this this website conations in fact nice funny information too.|

фильмы онлайн для телефона

This design is wicked! You most certainly know how to keep a reader amused. Between your wit and your videos, I was almost moved to start my own blog (well, almost…HaHa!) Great job. I really enjoyed what you had to say, and more than that, how you presented it. Too cool!|

I just could not leave your website before suggesting that I actually enjoyed the usual info a person supply to your visitors? Is going to be back frequently in order to check out new posts|

I am in fact pleased to read this weblog posts which carries tons of useful information, thanks for providing these information.|

Buy Valdecoxib online

site

site

смотреть онлайн бэтмен против супермена

Enjoyed the post

Thanks for the post

Awesome post

Good post

whoah this blog is wonderful i like reading your articles.

Stay up the great work! You know, lots of persons are

looking around for this info, you could help them greatly.

I consider something genuinely special in this web site.

medunitsa.ru Medunitsa.ru

фильмы онлайн смотреть музыка сериалы видео

Wow, amazing blog format! How long have you been blogging for? you made blogging look easy. The total glance of your site is great, as smartly as the content!

1016

Excellent post. I used to be checking constantly this blog and I’m inspired! Extremely useful information specially the final phase 🙂 I maintain such information a lot. I used to be seeking this particular information for a very long time. Thank you and best of luck.

I genuinely appreciate your work, Great post.

Когда

Someone necessarily help to make severely posts I would state. That is the very first time I frequented your website page and up to now? I amazed with the analysis you made to make this particular publish extraordinary. Fantastic job!

You completed several good points there. I did a search on the topic and found nearly all people will go along with with your blog.

Respect to website author, some excellent selective information.

Merely wanna comment on few general things, The website style and design is perfect, the articles is real wonderful. “War is much too serious a matter to be entrusted to the military.” by Georges Clemenceau.

I believe this website has some rattling superb info for everyone : D.

I do agree with all the concepts you’ve presented in your post. They are really convincing and will certainly work. Nonetheless, the posts are very quick for newbies. May you please prolong them a little from subsequent time? Thanks for the post.

I’ve been exploring for a little bit for any high quality articles or weblog posts in this kind of house . Exploring in Yahoo I finally stumbled upon this web site. Studying this info So i am happy to convey that I’ve an incredibly good uncanny feeling I came upon just what I needed. I most surely will make sure to don’t fail to remember this website and provides it a glance regularly.

I really enjoy examining on this internet site, it contains wonderful posts.

Having read this I thought it was very informative. I appreciate you taking the time and effort to put this article together. I once again find myself spending way to much time both reading and commenting. But so what, it was still worth it!

Hey very nice blog!! Man .. Beautiful .. Superb .. I’ll bookmark your web site and take the feeds alsoKI am happy to seek out so many helpful information here within the submit, we want work out more strategies in this regard, thank you for sharing. . . . . .

Greetings! Quick question that’s totally off topic. Do you know how to make your site mobile friendly? My website looks weird when browsing from my apple iphone. I’m trying to find a template or plugin that might be able to fix this issue. If you have any recommendations, please share. With thanks!

It’s actually a great and helpful piece of info. I’m satisfied that you shared this helpful information with us. Please keep us informed like this. Thank you for sharing.

Merely wanna remark that you have a very nice internet site, I like the design it really stands out.

After study a few of the blog posts on your website now, and I truly like your way of blogging. I bookmarked it to my bookmark website list and will be checking back soon. Pls check out my web site as well and let me know what you think.

Great write-up, I?¦m regular visitor of one?¦s site, maintain up the nice operate, and It’s going to be a regular visitor for a lengthy time.

Deference to article author, some great entropy.

Hey There. I found your blog using msn. This is a really well written article. I will make sure to bookmark it and come back to read more of your useful information. Thanks for the post. I’ll definitely comeback.

I do agree with all the ideas you’ve presented in your post. They are really convincing and will definitely work. Still, the posts are very short for newbies. Could you please extend them a bit from next time? Thanks for the post.

Good day! I simply wish to give an enormous thumbs up for the good data you have right here on this post. I will likely be coming back to your blog for extra soon.

I have been browsing on-line more than 3 hours today, yet I by no means discovered any attention-grabbing article like yours. It’s beautiful price enough for me. Personally, if all web owners and bloggers made excellent content material as you probably did, the web can be much more useful than ever before. “When the heart speaks, the mind finds it indecent to object.” by Milan Kundera.